San Francisco Real Estate Market Update – May 2024

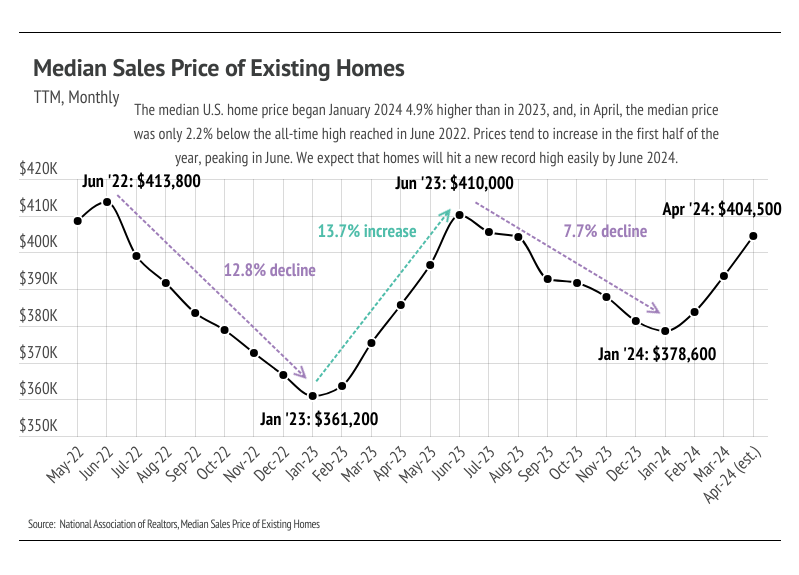

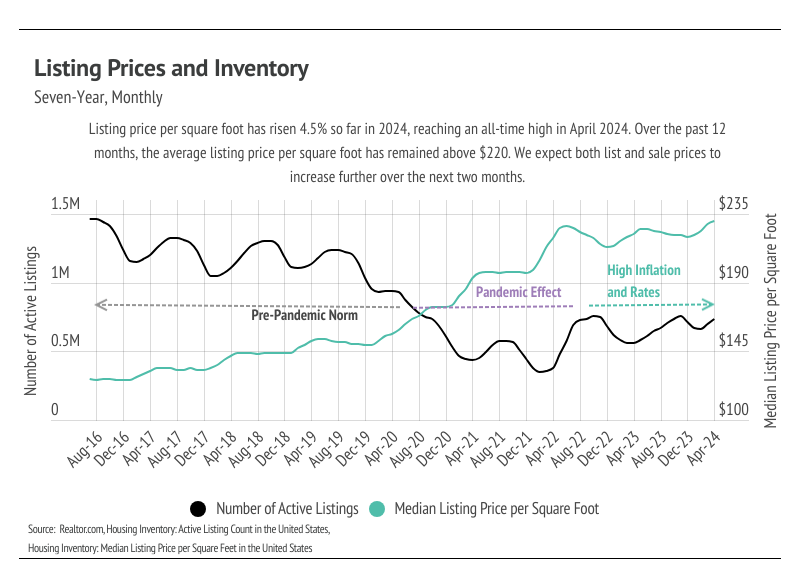

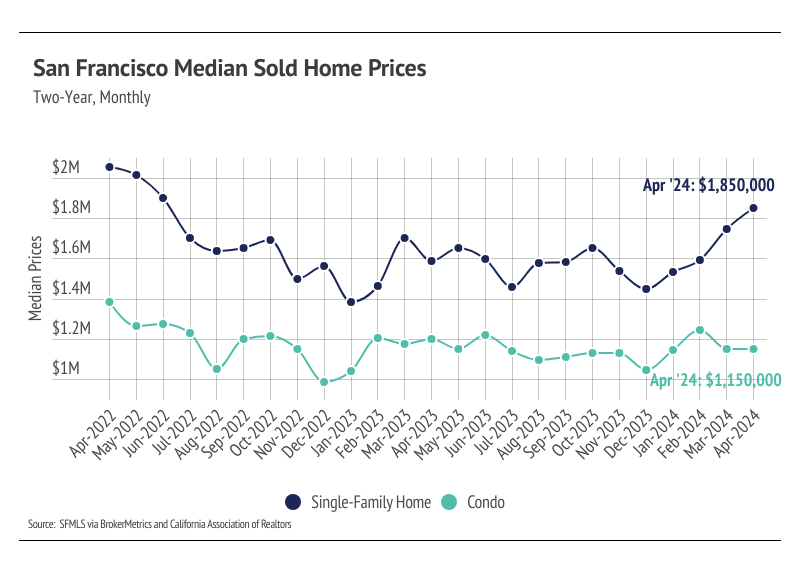

Prices have already risen 6.8% over the past three months, landing only 2.2% below the all-time high reached in June 2022. Additionally, the median list price per square foot hit an all-time high in April 2024.

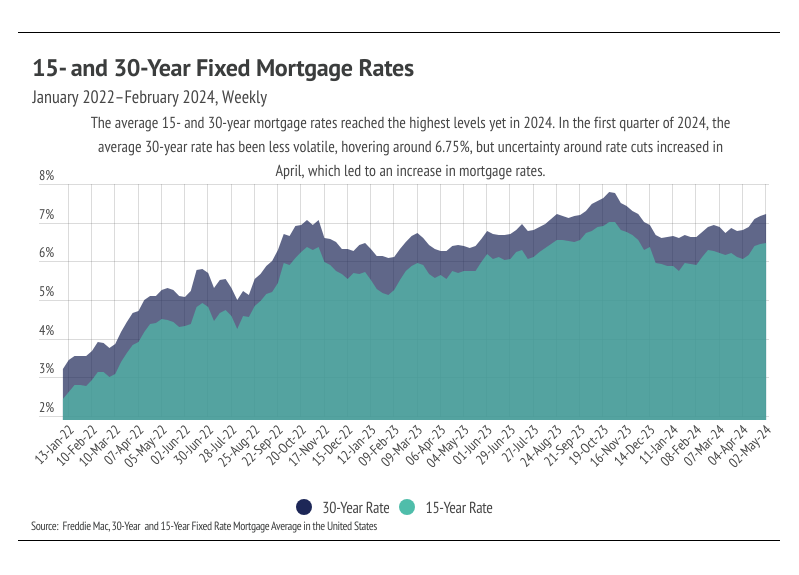

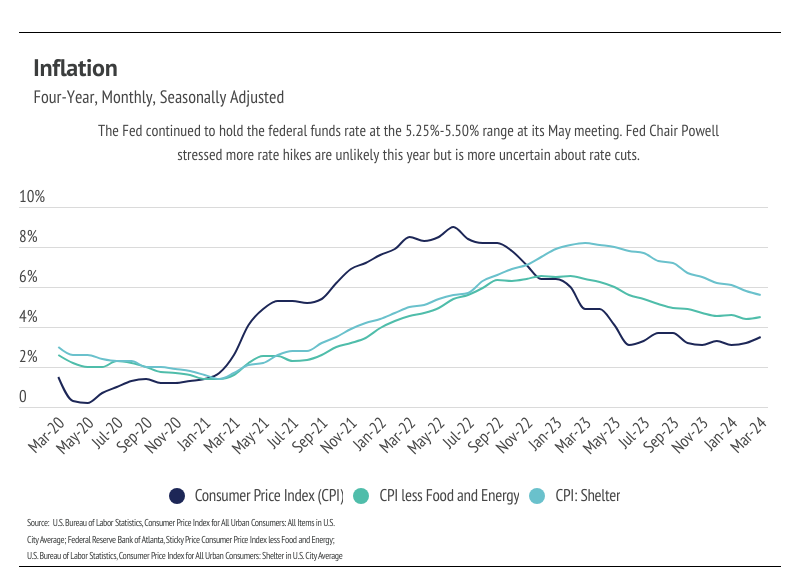

Mortgage rates rose nearly a half a percentage point in April due to changing Fed rate cut expectations, hitting the highest level yet in 2024. The Fed has expressed that inflation is taking longer to settle at 2% than originally expected, so higher rates will likely be here for most — if not all — of 2024.

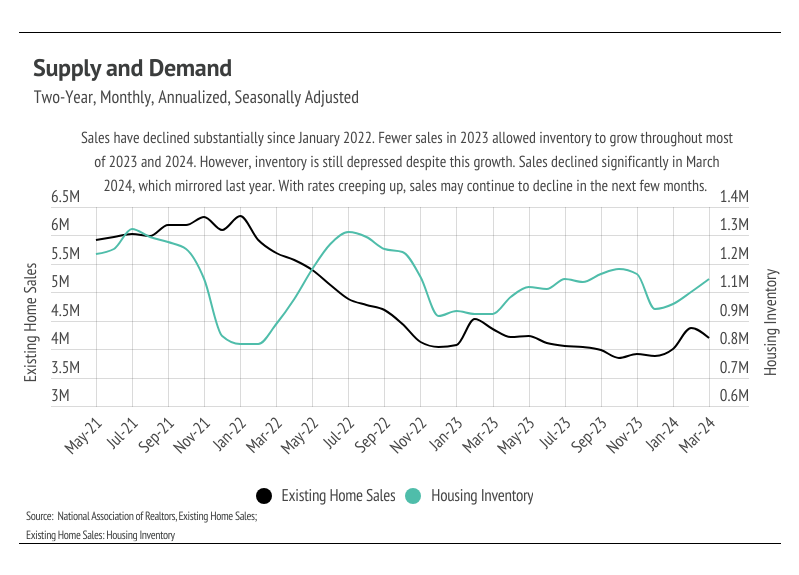

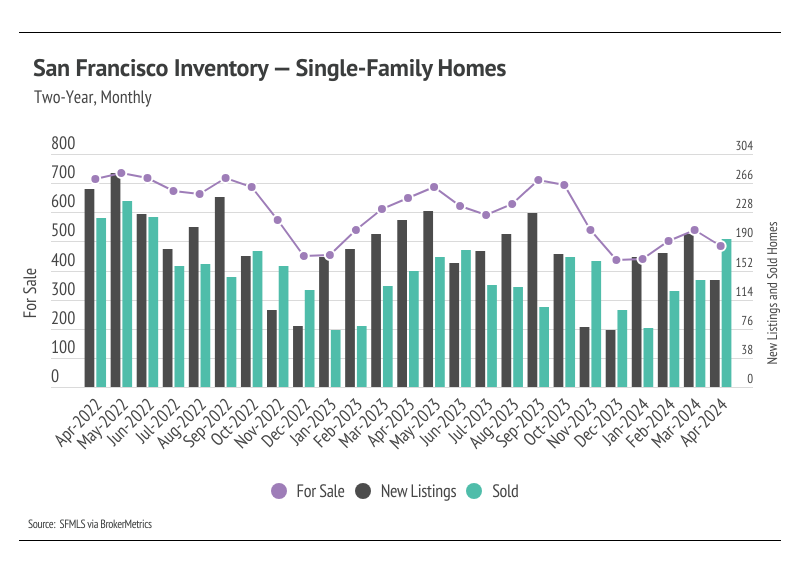

Sales fell 4.3% month over month, and inventory rose 4.7%. The combination of rising prices and interest rates priced buyers out of the market, which dropped sales.

The average 30-year mortgage rate began the year at 6.62%, marking the start of the third year mortgage rates have been elevated. However, the rate expectations for 2024 in January were far different from those today. In January, inflation was still trending lower and economists were predicting rate cuts as early as March. Unfortunately, the inflation rate stopped falling around 3%, never quite reaching the 2% target, which has caused the Fed to delay cutting the federal funds rate, which indirectly, but significantly, influences credit markets. The past two months, in fact, inflation has increased year over year, which isn’t ever going to move the timetable for rate cuts earlier.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

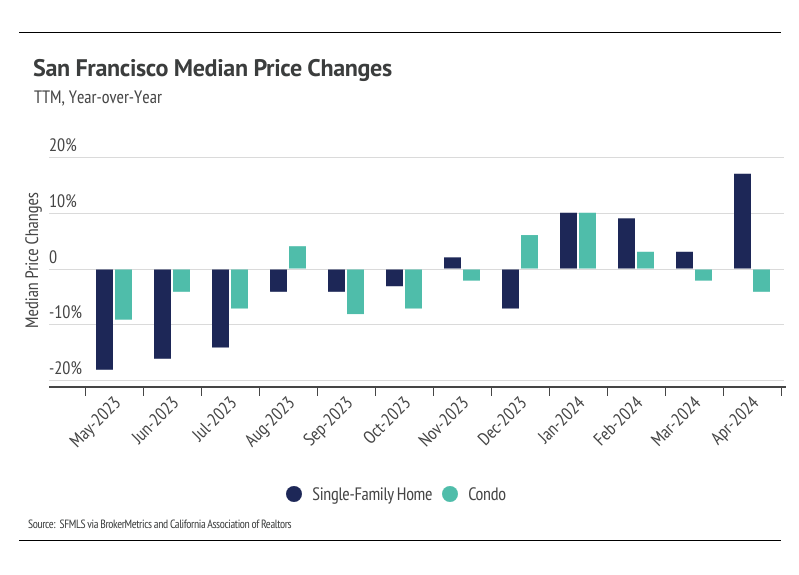

Median single-family home and condo prices rose meaningfully from December 2023 to April 2024, up 27.6% and 10.6%, respectively. Year-over-year prices also appreciated for single-family homes, up 16.5%

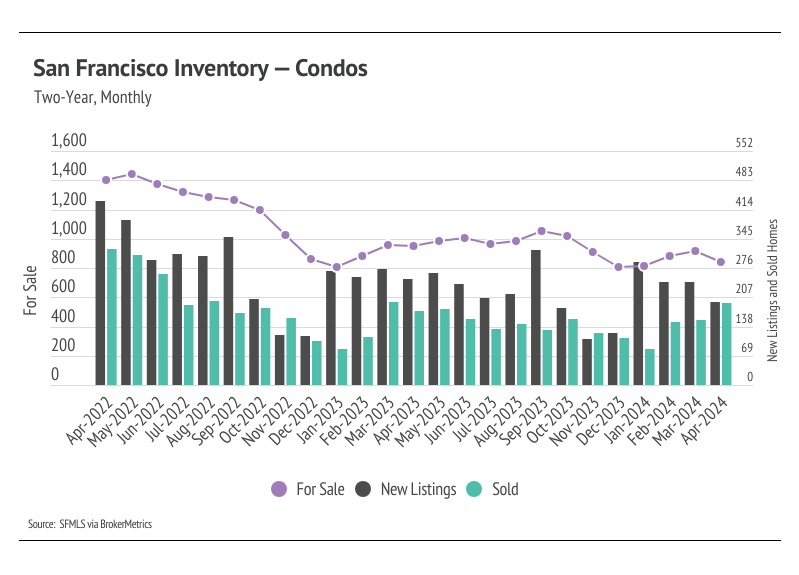

Active listings in San Francisco fell 7.6% month over month. Both single-family home and condo inventory are once again near record lows, as sales increased and new listings fell.

Months of Supply Inventory fell from January to April 2024, indicating that buyer competition is ramping up. MSI implies a sellers’ market for single-family homes and a balanced market for condos.

In San Francisco, home prices haven’t been largely affected by rising mortgage rates after the initial period of price correction from May 2022 to July 2022. Since July 2022, the median single-family home and condo prices have hovered around $1.5 million and $1.2 million, respectively. However, for single-family homes that trend may be changing. From December 2023 to April 2024, the median single-family home price rose significantly, up 28%. Year over year, the median price rose 17% for single-family homes, but fell 4% for condos. We expect prices to rise as more sellers come to the market. Additionally, inventory is so low that rising supply will only increase prices as buyers are better able to find the best match. More homes must come to the market to get anything close to a healthy market.

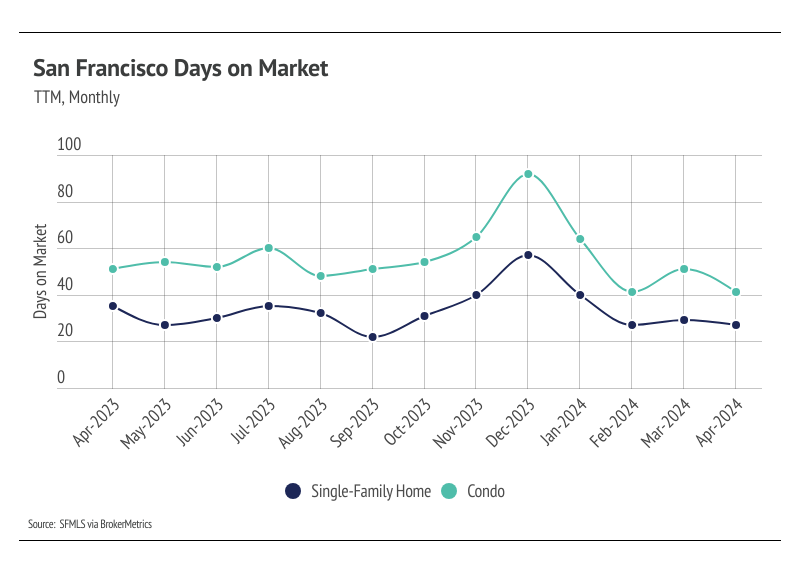

High mortgage rates soften both supply and demand, but homebuyers seemed to tolerate rates above 6%. Now that rates are above 7%, sales may slow slightly in the next couple of months, which isn’t great for the market, but isn’t it terrible, either, as it may allow inventory to build in a massively undersupplied market.

Since the start of 2023, single-family home inventory has followed fairly typical seasonal trends, but at a significantly depressed level, while condo inventory has been in decline since May 2022. Low inventory and fewer new listings have slowed the market considerably. Typically, inventory peaks in July or August and declines through December or January, but the lack of new listings prevented meaningful inventory growth. Last year, sales peaked in May, while new listings and inventory peaked in September. New listings have been exceptionally low, so the little inventory growth throughout the year was driven by fewer sales. In November and December 2023, new listings dropped significantly without a proportional drop in sales, causing inventory to fall to an all-time low in December, which further highlights how unusual inventory patterns have been over the past year. However, new listings in January 2024 rose 134% month over month.

The number of new listings coming to market is a significant predictor of sales, and the new listings in January led to a 68% sales increase in February. Both inventory and new listings declined from March to April, but sales rose considerably, up 33%. Year over year, inventory is down 16% and new listings are down 25%, but sales are up 20%. Demand is clearly coming back to San Francisco, but more supply is needed for a healthier market.

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The San Francisco market tends to favor sellers, at least for single-family homes, which is reflected in its low MSI. However, we’ve seen over the past 12 months that this isn’t always the case. MSI has been volatile, moving between a buyers’ and sellers’ market throughout the year. From January to April, MSI declined significantly, indicating that single-family homes shifted from balanced to favoring sellers, and condos moved from favoring buyers to balanced.

Stay up to date on the latest real estate trends.

April 29, 2025

March 27, 2025

February 27, 2025

January 23, 2025

December 18, 2024

November 18, 2024

October 17, 2024

September 16, 2024

August 28, 2024

You’ve got questions and we can’t wait to answer them.